ISA: All Set with Just 3 Baskets!

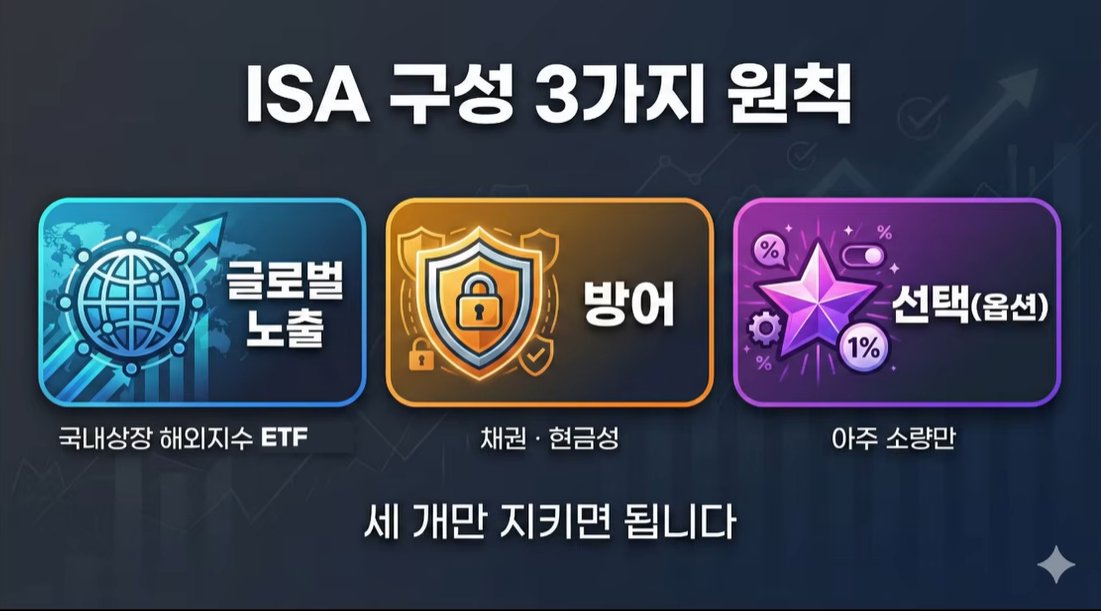

Principles and Core Direction of ISA Investment

Image Source: YouTube Channel Yeo Woon-bong Wealth Academy

The Dominance of ISA Brokerage Accounts: Rather than relying on trust or discretionary ISA accounts offered by banks and brokerages, we highly recommend choosing a brokerage-type ISA from a securities firm. This option allows you to directly manage individual stocks and a broad spectrum of financial products.

Direct Overseas Purchases Prohibited; Use Indirect Methods: Within an ISA, you cannot directly purchase stocks listed on foreign exchanges (e.g., Apple, Tesla) or US-listed ETFs. However, by utilizing domestically-listed overseas index ETFs, you can achieve the exact same effect of global asset allocation.

Simplifying Asset Allocation: Do not overcomplicate your portfolio by packing it with dozens of different assets. Just three baskets are more than enough: Global Growth Exposure (Stocks) + Defense (Bonds/Cash) + Personal Preference (Optional).

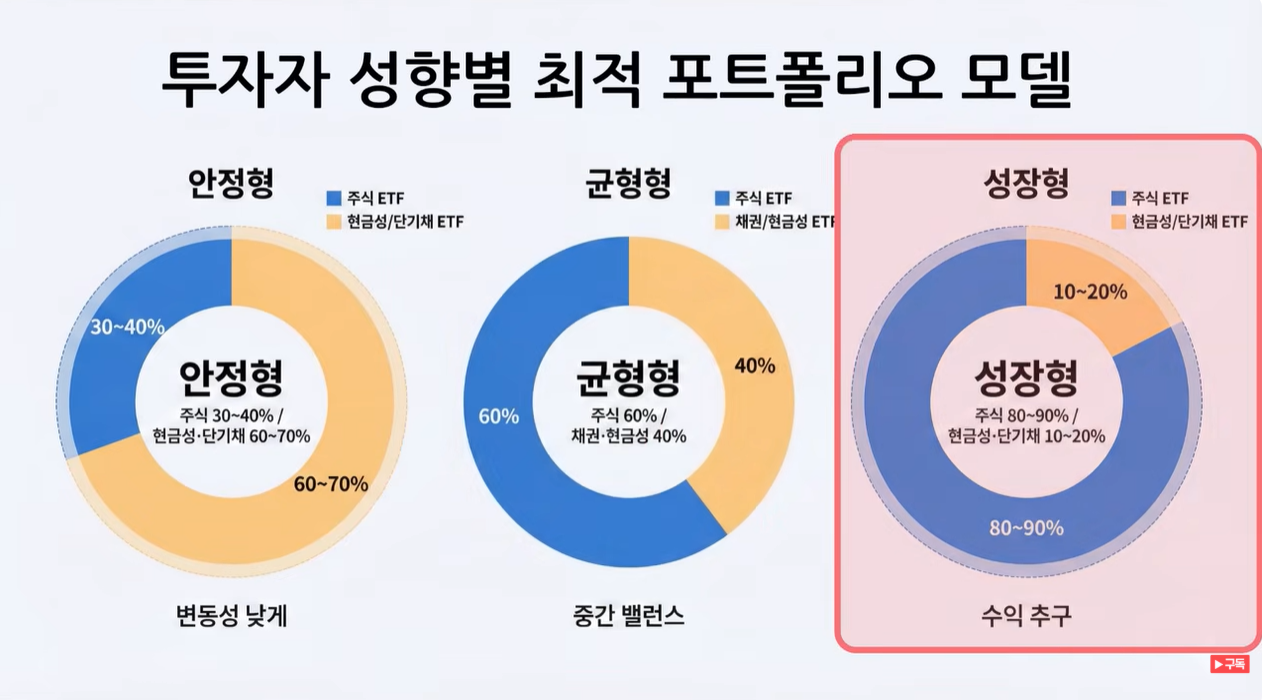

Diagnose Your Investment Persona: Safety, Balance, or Growth

Image Source: YouTube Channel Yeo Woon-bong Wealth Academy

Before diving into investing, it is crucial to assess your investment temperament by answering these three fundamental questions:

Investment Horizon: "Can I leave this money untouched for at least 3 years, or ideally for over 10 years?"

Result: Shifts your bias toward a Growth approach.Volatility Tolerance: "If my account balance drops by -20%, would I lose sleep over it?"

Result: Shifts your bias toward a Safe or Balanced approach.Crisis Response: "When a market crash occurs, can I view it as a clearance sale and buy even more?"

Result: Highlights the need for a Growth engine while maintaining a robust defensive shield.

Core Framework: The Magic Three Baskets and Proportions by Persona

Do not obsess over specific ETF names or ticker codes. The only thing that matters is understanding what role each asset plays in your portfolio.

🧺 Basket 1: The Growth Engine (The Main Compounder)

Role: To heavily compound and significantly grow your wealth over the long term.

Assets: ETFs tracking major US indices (S&P 500), US tech indices (NASDAQ), or all-world equity indices.

🧺 Basket 2: The Shield (The Emotional Anchor & Ammunition Depot)

Role: To protect your portfolio from being decimated during market crashes and to serve as dry powder to buy equities when they become cheap.

Assets: Short-term bond ETFs, cash-equivalent/money-market (CD rate, etc.) ETFs, and high-quality fixed-income ETFs.

🧺 Basket 3: The Optional Selection (The Personal Preference Corner)

Role: A minor bonus section designed to satisfy personal interests and add a bit of flavor to your investing.

Assets: High-dividend yield styles, REITs (real estate), or specific thematic ETFs you have closely followed.

Note: Keep greed in check and ensure this remains a very small fraction of your portfolio.

📊 Portfolio Blueprint Guidelines by Investment Persona

The asset allocation metrics below are not absolute answers; rather, they serve as guidelines designed to prevent costly amateur mistakes. Configure your allocations mechanically based on your diagnosis.

Investment PersonaGrowth Engine (Equities)The Shield (Bonds/Cash)Optional Selection (Preferences)Key Characteristics

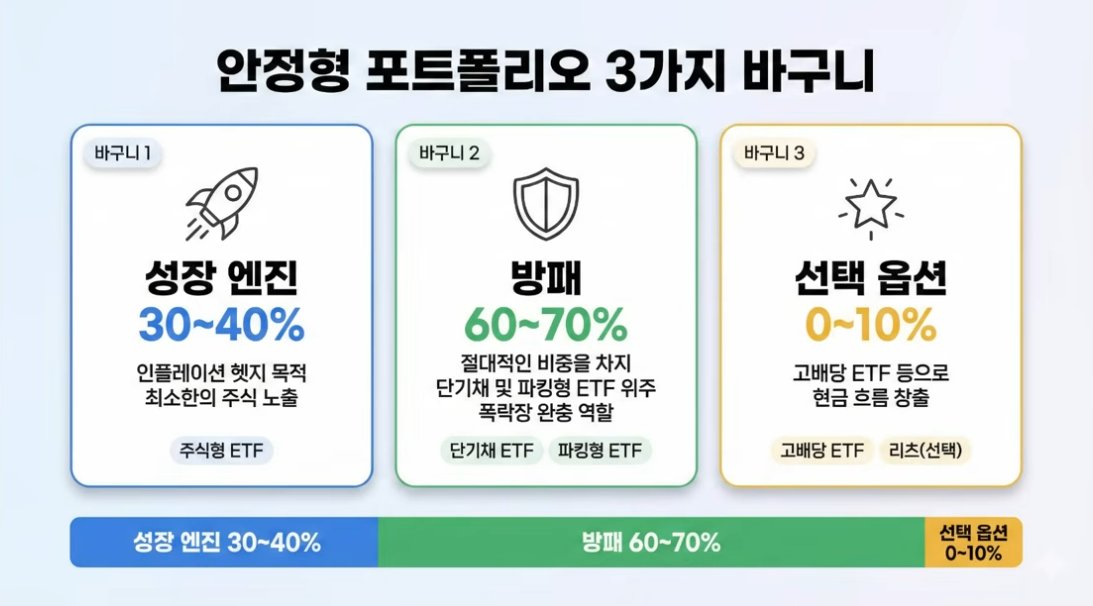

[Safe Type]

Image Source: YouTube Channel Yeo Woon-bong Wealth Academy

※ Sleep is the top priority

Prioritizes defensive resilience over high returns. Designed to help investors weather major market crashes with peace of mind over the long haul.

Case Study: A self-employed investor in their 50s with irregular income. Needs a thick defensive shield to withstand volatile cash flows.

[Balanced Type]

Image Source: YouTube Channel Yeo Woon-bong Wealth Academy

※ The highly recommended textbook standard

Achieves a flawless harmony between wealth accumulation and defense. This structure is engineered to prevent beginners from throwing in the towel halfway.

Case Study: A salaried corporate worker in their 40s. Facing upcoming education expenses for children and completely new to investing. Recommended setup: 60% equities, 40% shield, rebalancing once a month.

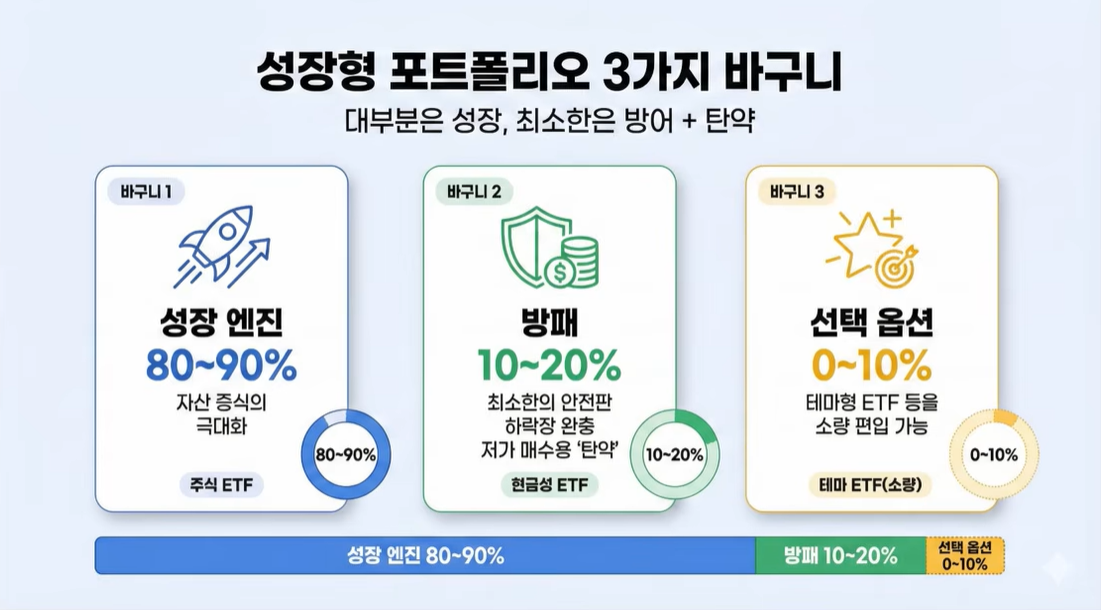

[Growth Type]

Image Source: YouTube Channel Yeo Woon-bong Wealth Academy

※ Ready to ride out extreme volatility

A structure where the growth engine takes center stage. However, retaining a minimum of 10% to 20% in the shield is mandatory to exploit buying opportunities during a crash.

Case Study: A young professional in their 30s capable of long-term investing and handling high volatility. Must still preserve 10% to 20% in defensive assets.

5-Step Checklist for Selecting Real-World ETFs

If you are paralyzed by choice when looking at the sea of available ETF products, evaluate them systematically using these five steps:

Check 1. Underlying Index (What does it track?): The underlying index dictates your ultimate returns far more than the product name. Always verify whether it tracks the S&P 500, a specific bond index, or something else.

Check 2. Total Expense Ratio (Are the fees cheap?): This is the hidden cost that quietly erodes your capital every year. A seemingly minor difference of 0.1% versus 1% transforms into a massive compounding disaster—or blessing—over a 10-year horizon. Always opt for the lowest fee structure.

Check 3. Liquidity (Is the trading volume high?): Choose ETFs with substantial daily trading volume and large assets under management (AUM). High liquidity ensures you can enter and exit positions immediately at fair market value whenever you want.

Check 4. Distribution Policy (Growth vs. Cash Flow): Dividends are not free bonuses; they are simply a portion of your total asset value being carved out and handed to you as cash. If you are in the wealth-accumulation phase, prioritize growth-oriented index ETFs over dividend-heavy products.

Check 5. Currency Hedging (Look for the 'H' tag):

Currency Unhedged (Standard): Suitable if you are investing for 5 to 10 years and are willing to embrace fluctuations in foreign exchange rates (such as shifts in the value of the US dollar). (Recommended)

Currency Hedged (Indicated by an 'H' at the end of the product name): Choose this if you absolutely cannot tolerate your asset value fluctuating due to swings in exchange rates.

⚠️ Three Capital Sins to Avoid in an ISA Account

These are the three primary culprits that ruin beginner portfolios. Avoiding these mistakes alone will instantly place you in the top 20% of all investors.

Sin 1. Going All-In on Thematic ETFs (e.g., Secondary Batteries, Semiconductors, Metaverse)

Thematic funds skyrocket during hype cycles but can take years to recover once the bubble bursts. Because an ISA is an account meant to be maintained for at least 3 years, it is fundamentally incompatible with short-term, volatile trends. If you must speculate, limit it to less than 10% within your "Optional Selection" basket.

Sin 2. Long-Term Holding of Leveraged (2x, 3x) ETFs

Leveraged products do not double or triple long-term absolute returns; they multiply daily volatility by two or three. When markets trade sideways or experience choppy volatility, a phenomenon known as volatility drag erodes your capital. Consequently, even if the underlying index returns to its original level, your account balance will end up deep in the red. This makes leverage toxic for a long-term compounder like an ISA.

Sin 3. Unconditional Obsession with Dividend Distributions

Attempting to build a growth-oriented portfolio to aggressively compound wealth while simultaneously draining cash via dividend payouts is equivalent to trying to sprint forward while leaking fuel. This only complicates your portfolio and breaks the magic of compounding. Keep your objectives crystal clear and separate: choose either asset growth or income generation, but do not mix them haphazardly.

The Investing Routine: The Only Way Amateurs Can Beat the Market

Beginners do not fail because they lack financial knowledge; they fail because they succumb to emotions (fear and greed). The key to success is establishing a mechanical routine that entirely removes human emotion from the equation.

Fix a Specific Monthly Date: Pick one specific day every month, such as the 25th or the final business day.

Block Out Market Forecasts: On that designated day, completely tune out market commentary, YouTube financial news, and sensational headlines predicting either imminent market crashes or historic highs.

Execute Mechanical Proportional Buying: Regardless of whether the market surged or plummeted, quietly and stubbornly purchase your assets according to your pre-set allocation ratios (e.g., Balanced Type: 60% equities to 40% bonds). By consistently buying during both market highs and lows, you naturally achieve dollar-cost averaging, optimizing your average purchase price over time.

The Ultimate Life Hack for Salaried Workers: Set up an automatic transfer to your ISA account for the day after your payday, and immediately buy your ETFs according to your designated ratios. This automated system is the open secret of top-tier investors who build wealth the fastest.

Frequently Asked Questions (FAQ)

💬 Q1. How many different ETFs should I buy?

A. Packing your portfolio with a laundry list of assets is not a sign of expertise; it is a critical flaw. Overly complex portfolios become impossible to manage, inevitably driving you toward emotional trading. It is best to keep it clean: 1 to 2 Growth Engines, 1 Shield, and 0 to 1 Optional Selection. A total of 2 to 4 distinct funds is plenty.

💬 Q2. Can I just put 100% of my money into a single US index ETF like the S&P 500?

A. It is technically possible. However, going all-in leaves you vulnerable during a brutal market downturn. Emotional fatigue often causes investors to panic-sell at the absolute bottom. Incorporating even a modest 10% to 20% defensive shield (bonds/cash) provides the psychological cushioning needed to sustain your investment strategy over the long run.

💬 Q3. Doesn't the market seem overvalued right now? Shouldn't I wait for a better entry point?

A. Timing market tops and bottoms is a feat reserved for the divine. Instead of wasting energy trying to time the market, executing a monthly, fixed-date recurring investment perfectly dilutes the risk of buying at a market peak.

💡 Summary Checklist

Remember the three core baskets: Growth, Shield, and Optional Preference.

Lock in your allocation ratios based on your persona: Safe, Balanced, or Growth.

Steer clear of the three capital sins: thematic concentration, long-term leverage, and dividend obsession.

Establish a fixed monthly mechanical routine to execute your purchases automatically.

Article Source:

ISA, Your Portfolio is Perfect with Just 'Three' of These ETFs

Support the independent voice of Ludens Times

Today's Reflection

Record your daily action inspired by today's article.

The Ludens Times Digest

Get our latest inspirations delivered straight to your inbox.